Having looked at how Coin and Google Wallet use different approaches to presenting a wallet experience that can utilize multiple credit cards, this post looks at how they compare against traditional plastic cards in security. Specifically we focus on two common threats both technologies face:

- Theft/loss of card. This also includes temporary access to the card by the adversary, such as settling a bill at a restaurant when the server gets full access briefly. (Although NFC payments are not typically used in this setting, we can extrapolate to the equivalent hypothetical scenario when the phone is tapped against a hostile point-of-sale terminal.)

- Data-breach occurring at a merchant where the card is used, or upstream at the payment processor used by the merchant. Target breach past October and the more recent PF Chang’s breach are examples of the first scenario, while the 2012 attack against Global Payments falls into the latter category.

Theft or loss of device

While Coin is not released yet, from the FAQ and a demonstration video one can surmise two features:

- The magnetic stripe does not carry card information at all times. It is only visible during transaction time, limiting the window of exposure. If bad guys get hold the card outside that window, there is nothing to read out of the stripe directly. (Contrast this with traditional plastic cards, where the information can be read at any time.)

- Physical proximity to the phone is required. The card locks up when it is out of range, measured by Bluetooth signal-strength. A corollary is that theft of the card alone is not useful directly, unless the thief also managed to get hold of the phone.

There is a caveat associated with both of these mitigations: they rely on the tamper-resistance of the hardware powering Coin. After all the track-data is still present inside the card, lurking somewhere on persistent storage; it is just not reflected on the dynamic stripe. If an attacker can extract this information by targeting the storage, they could obtain track data for all stored cards. Similar to the problem of extracting the cryptographic keys embedded in a chip & PIN card, this is an attack against the physical tamper-resistance of the hardware. At the moment little is known about the hardware inside Coin. There are standard benchmarks for evaluating the physical security of cryptographic hardware, such as the United States government’s FIPS 140-2 standard and its European counterpart Common Criteria. Popular models of smart-cards often boast a FIPS 140 or CC certification level, and EMV payment applications typically require such a certification before the hardware can be used to implement payment protocols. It is unclear if similar requirements will apply to Coin.

For Google Wallet, the main defense against theft is a PIN. Tap-and-pay is only possible when the application was unlocked “recently” by entering the correct PIN, based on a configurable time interval. In earlier incarnations of the product that leveraged the embedded secure-element, this period defaulted to 5 minutes. More recent versions based on host-card emulation extend that to 24 hours. That means if the user made a transaction recently the device is “armed” and ready for future purchases, by simply turning on the screen. Even unlocking the phone itself– such as by entering a pattern or PIN– is not required. Payments only require that the display is on, which is used as the signal to power-on the NFC controller.

Tamper-resistance used to be an important part of the threat model for earlier versions of Google Wallet, since long-lived cryptographic keys were stored on the embedded secure element. Physical attacks against the SE could result in the extraction of these keys, allowing “cloning” of the card. (Unlike Coin however, SE hardware has proven track record and pedigree: both NXP SmartMX and Oberthur/ST33 family have underwent Common Criteria evaluation.) But later iterations of Wallet dropped support for SE in favor of NFC host card emulation, managing payment credentials on the main Android application processor. While there is no pretense of tamper-resistance on that platform, HCE also changes the key management model for payments. Instead of trying to secure a single key over an extended period of time, new keys are periodically downloaded from the cloud on-demand, after authenticating the user. This also serves as a useful mitigating factor against theft of the device. Even sophisticated attackers who can extract the secrets associated with an Android application will not be able to create a functional replica.

Skimming and compromised merchants

Google Wallet fares better than Coin against skimming and hostile point-of-sale terminals. Recall that while Coin card can suppress any data from appearing on the magnetic stripe until the moment of transaction, when that swipe does eventually happen, the data surrendered to the reader will be an identical clone of one of the user’s existing cards. Coin FAQ admits as much:

” A Coin is no less susceptible than your current cards to other forms of skimming that capture data encoded in the magnetic stripe as the card is swiped.”

By contrast NFC payments produce a “simulated” track-data with two components that change for each purchase: an incrementing transaction counter and a dynamic card-validation-code or CVC3 computed jointly by the reader and wallet application in a challenge-response protocol. In other words the track-data is constantly changing, unlike the static picture presented by Coin to every cash register. Even if an attacker commands a malicious NFC terminal and observes several different CVC3 values, they can not recreate future CVC3 values necessary to successfully authorize a different transaction. (More details about the construction of the simulated mag-stripe appear in earlier posts about a hypothetical scenario: paying with NFC at Target when the retailer was still under attack– hypothetical because Target has not rolled out NFC.)

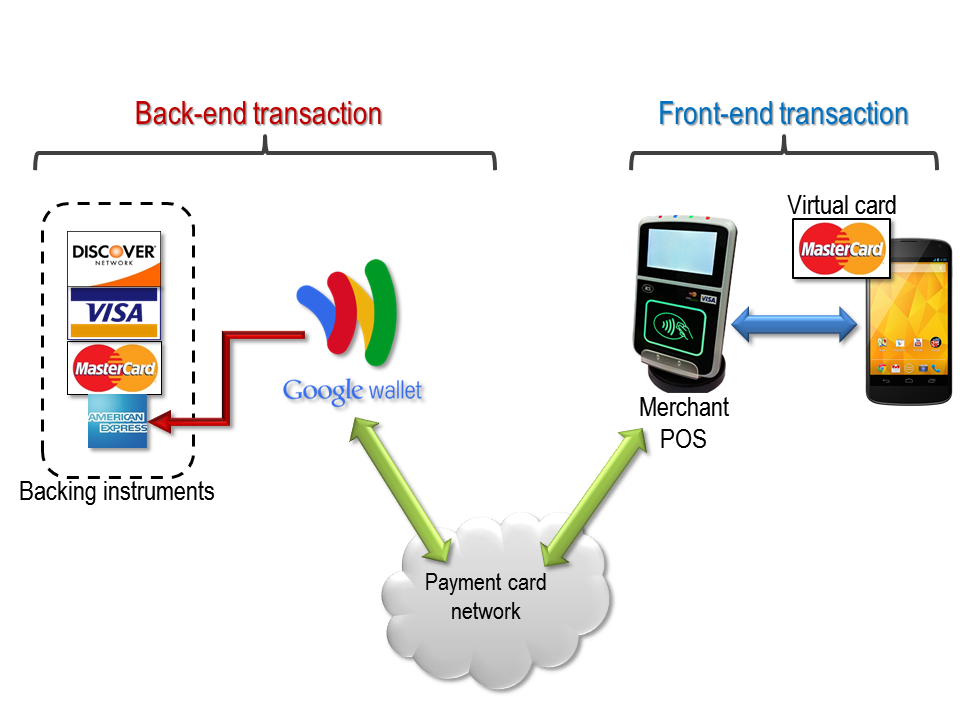

Even more importantly, the virtual card used by Google Wallet to redirect payments is completely decoupled from the “real” plastic cards the consumer added to their wallet as funding sources. Nothing about the original cards– not the cardholder name, expiration date or even the types of cards Visa/MC/AmEx/Discover present in the wallet– can be inferred from use of the virtual card. This in itself is very useful when recovering from a breach: even if merchant terminals had been completely compromised a la Target, there is no need to cancel and reissue the physical credit cards of customers who paid with Google Wallet. The only “card” at risk is the virtual one issued by Google for proxying transactions, and it is Google’s problem to reissue that card– which is as easy as provisioning a new one over the air to the phone. Banks who issued the “real,” tangible cards safely hidden on the other side of those transactions need not worry about shipping new pieces of plastic to their customers.

CP

You must be logged in to post a comment.