Stalemate

Previous two posts [part I, part II] reviewed the counter-intuitive dynamics of how payment networks externalize and disperse fraud, by setting issuers and merchants against each other over direct losses. Those actors in turn incorporate expected losses into cost of services rendered to consumers.

As long as fraud costs are predictable and already factored into existing prices, they can be viewed as the cost of doing business. Granted such losses incorporate an element of chance and perfect projections are not possible. Some years it may be less than projected, adding to the bottom line, while other years “black-swan” events such as the Target breach could result in much higher losses than expected. But as long as risks are manageable, it creates a stalemate in the system, one that goes a long way to explain why card networks have not particularly motivated to institute a crash-upgrade to EMV across the board. Issuers and merchants are locked into an archaic technology— the ubiquitous magnetic stripe and CVC2 codes— which are trivially defeated by vanilla PC malware, card-skimmers, compromised point-of-sale terminals and phishing scams. Yet the cost of upgrading point-of-sale terminals (and payment-processor connections— this one is not a simple matter of attaching an NFC reader and relying on backwards compatibility) may exceed projected reductions in fraud. As late as 2012 Glennbrook stated:

“In the US the common assumption is that the current level of counterfeit card fraud is too low to merit an industry-wide investment in EMV technology.”

Placing incentives on the right actors

That brings up the question about who should be paying for improving security and reducing fraud in the system. There is a certain logic to exempting card-holders out of the fight around who gets to absorb fraud losses: there is very little actionable for individuals in the way of reducing risk. In fact most “intuitive” responses can be counter-productive for the overall payments ecosystem: avoiding plastic in favor of cash— as consumers were reportedly doing in response to recent breaches— may indeed reduce fraud figures but only at the expense of losing issuer and revenue. (It may also increase cash losses which unlike credit-card fraud is not distributed to other individuals in the risk pool. As consumers in Greece noticed, when households began to stockpile cash and valuable, thefts and burglaries increased.)

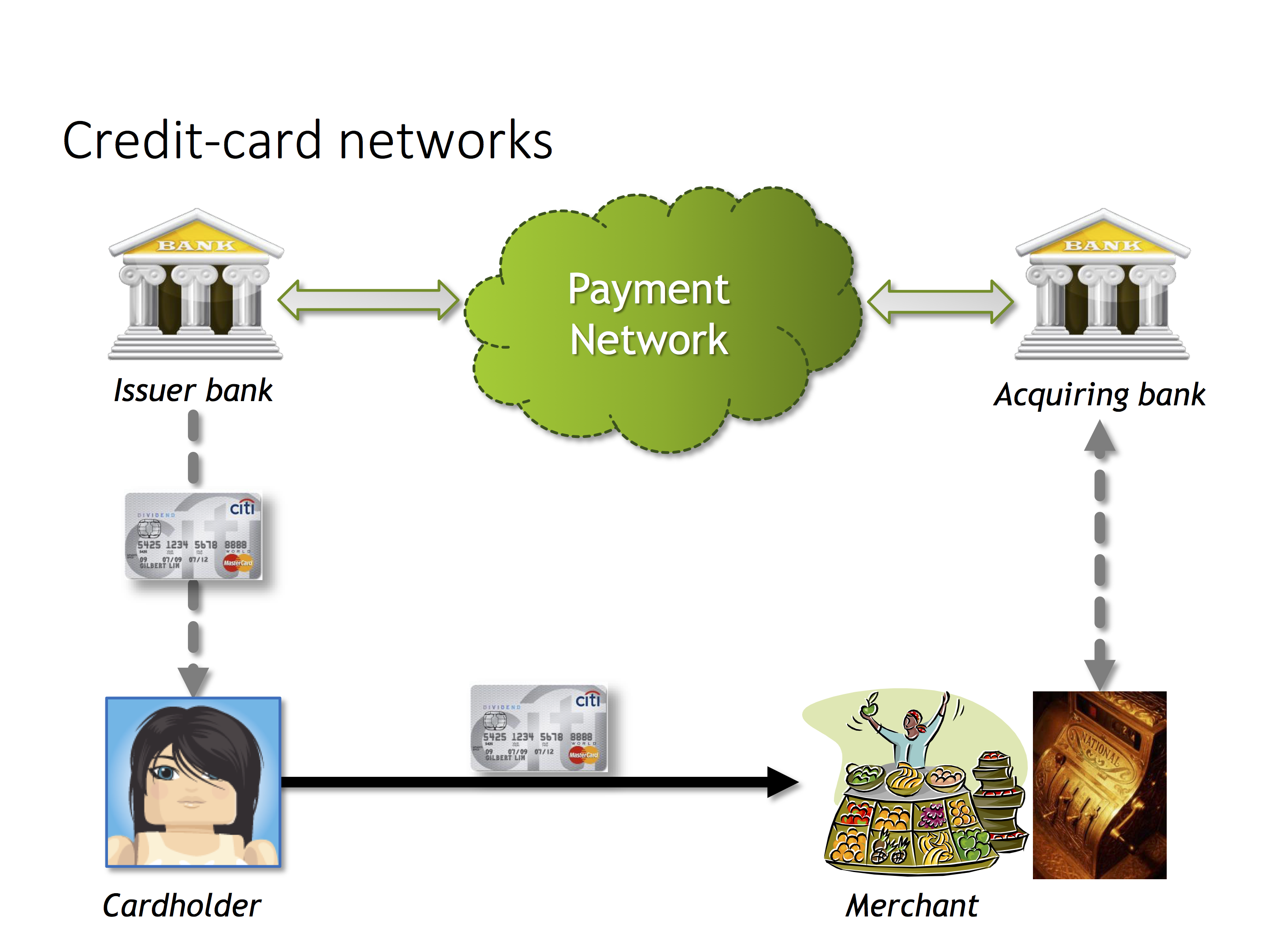

Issuers and acquirers have more direct control over the risk levers in a given transactions. Issuing bank has the one final say in authorizing every transaction, with knowledge of amount and some notion of merchant involved. To improve their odds, they develop or more commonly out-source sophisticated risk management systems that sift through the haystack of card-holder transactions in real-time and flag suspicious patterns. Similarly merchants can institute policies based on their level of risk tolerance. Examples for retail outlets include:

- Accepting thresholds set by networks for when signatures are required. Starbucks prefers to keep the line moving for smaller amounts, since quick customer service is critical in a volume business, but take time to pause on larger purchases

- Requiring a valid government-issued ID with name matching the payment card

- Prompting for additional card-holder information that can be checked during authorization process. Gas station pumps requesting ZIP code is the canonical example

Likewise e-commerce merchants subject to card-not-present risks can set certain policies such as:

- Collecting CVC2 codes for additional card verification (Interestingly many large merchants including Amazon did not do this for the longest time)

- Not shipping to PO boxes. These are easy to obtain and favored by shipping-mules to hide their true address

- Checking billing address during authorization against information entered by the customer

- Requiring additional verification when shipping address is different from billing address

All of these are actionable for the issuer/merchant and more importantly, decisions can be made independently by each actor. Set the rules too conservatively, and legitimate customers are driven away because their purchases are declined. Set them too liberally and an entire underground crew of professional crooks decide to prey on that merchant.

EMV deadline

Clearly something did change in the intervening years because Visa and MasterCard set a deadline of Oct 1st 2015 for EMV adoption in the US. The timing of the announcement coincided with the aftermath of large-scale breaches at Target and Home Depot. While correlation is not causation, one could speculate that card networks capitalized on the climate of heightened fear among consumers at the time to accelerate an EMV agenda which had been slow to gain traction until that point. Mainstream media also latched on a simplistic rhetoric that chip-and-PIN equals no more data breaches, creating a perfect environment to push EMV migration. With merchants backed into a corner too busy explaining why their shoddy security resulted in frequent data breaches, there would be no room for the type of careful cost/benefit analysis that has been otherwise the hallmark of risk management in payments.

So-called “upgrade” plan itself took the form of an ultimatum to issuers and merchants. Past the deadline, rules for disputing in-store transactions change. If the issuing bank had provided the customer with a chip&PIN card but the merchant terminal was only capable of swipe transactions, now it is the merchant who gets to eat the loss if that charge is later disputed by the card-holder. Conversely for those few situations when the merchant would have been on the hook, such as skimping on signed receipts in the interest of quick customer turnover, the bank may be stuck with the loss if the merchant POS had been upgraded for processing EMV transactions but customer card only had swipe capability. (Interestingly enough, if neither side had upgraded then business-as-usual rules apply. In that sense, not upgrading is the optimal outcome for both merchant/issuer when viewed as prisoner’s dilemma game, but the threat that the other side may “defect” would inspire both to settle for the more costly action of going through the upgrade.)

This is another great example of cost diffusion at work. Note that Visa and MasterCard are not on the hook for the vast majority of upgrade costs. The letters V and M in “EMV” may stand for their names but past research & development on EMV has become a historic sunk cost at this point. It is the issuing bank that must shell out for printing, personalizing and mailing millions of cards to their customers. Similarly the merchant is responsible for purchasing or leasing new equipment to accept EMV transactions. On the surface, consumers are off the hook again, much like their indemnification over fraudulent purchases. But to echo Robert Heinlein, TANSTAAFL: those issuer and merchant expenses be paid from somewhere. Absent any government subsidies to encourage better security— which have never played a significant role in this space— that source is the price of goods and services. Consumers will indirectly pay for this upgrade cycle too.

CP

You must be logged in to post a comment.